Could a federal ban on large institutional investors buying single-family homes actually make it easier for first-time buyers in San Antonio and New Braunfels to finally get under contract?

The short answer: possibly in very specific situations—but it won’t magically fix affordability on its own. While such a policy could reduce competition in certain investor-heavy pockets, the larger forces shaping affordability—housing supply, interest rates, and monthly payment pressure—still matter far more.

For buyers trying to cut through the headlines, here is what this proposal realistically means on the ground. For expert updates on Texas Hill County and New Braunfels Real Estate Market, contact Cody Posey – you dedicated specialist.

What Was Announced—and What Is Still Unclear

On January 7, 2026, President Donald Trump announced his intention to ban large institutional investors from purchasing additional single-family homes. The proposal is framed as a way to improve affordability for everyday buyers by limiting the ability of “Wall Street” to scoop up starter homes.+1

However, the most important detail is also the least defined: what qualifies as “large.” Without legislative language or enforcement guidelines, it remains unclear if this applies to companies owning 100 homes, 1,000 homes, or tens of thousands. For buyers searching for clarity around San Antonio Real Estate trends, this distinction matters more than the headline itself.

Financial markets reacted immediately, with stock prices for major rental operators dropping as much as 10% before stabilizing. This indicates the industry is taking the threat seriously, but federal housing policies tied to property rights often face prolonged legislative and legal paths.

Why This Issue Feels Personal in South Texas

Investor activity has not been theoretical in South Texas—it has been visible. During the pandemic surge, institutional buying spiked dramatically in Bexar County. Some reports showed that in 2021, nearly half of the homes sold in certain zip codes went to institutional buyers. That surge reshaped buyer experiences almost overnight: more cash offers, fewer contingencies accepted, and tighter closing timelines.

For many New Braunfels Housing Market participants, this period cemented the feeling that the deck was stacked against financed buyers. When you are competing against a corporate entity that can waive an appraisal, the playing field feels uneven.

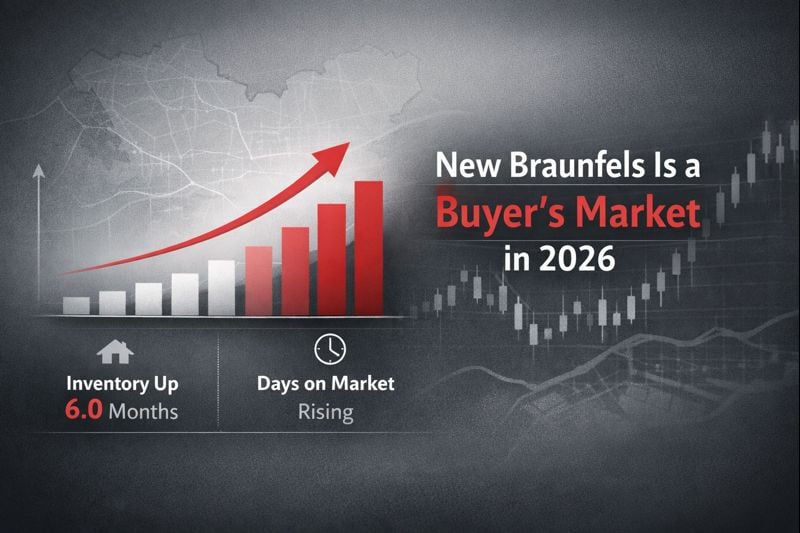

Current Market Data: Leverage is Already Returning

Here is the part most buyers overlook: you do not need a federal ban to gain leverage in today’s market. According to January 2026 data from the San Antonio Board of Realtors (SABOR), the market is already operating with more balance:

- Median Home Price: $309,990 (A shift reflecting more moderate price range activity).

- Active Listings: Approximately 17,043 (A 15% increase year-over-year).

- Months of Inventory: Standing at 6.1 months.

- Average Days on Market: 83 to 88 days.

In real estate terms, 6 months of inventory is the threshold for a “balanced” market. When inventory exceeds this, the leverage shifts to the buyer. This is the type of environment where Home Affordability strategies actually become usable—not theoretical. Buyers can now tour without rushing, compare options, and negotiate repairs.

Would a Corporate Buyer Ban Lower Prices?

Where You Might See a Difference

If a ban is written narrowly enough to reduce large investor participation, the most realistic benefits would be:

- Fewer cash-heavy competitors in the $200,000 to $350,000 price ranges.

- More sellers willing to accept FHA or VA financed offers.

- Greater acceptance of standard inspection and appraisal timelines.

Why Price Relief May Be Limited

Even if institutional investors are sidelined, Real Estate Data shows the central problem is supply. The U.S. is currently facing a structural shortage of millions of homes. Removing one category of buyer without increasing the number of homes built does not automatically lower prices—it often just reshuffles the competition among individual buyers.

Furthermore, some research suggests that if large investors stop funding new “build-to-rent” communities, total single-family construction could actually decrease, potentially making the supply shortage worse in the long run.

Practical Financing Tools for 2026

For buyers in South Texas, local and state programs can move the needle faster than national proposals. While waiting for policy changes, these tools can help bridge the gap in affordability today.

City of San Antonio HIP 120

The San Antonio Real Estate market is unique because of the Homeownership Incentive Program (HIP 120). For eligible buyers, this program offers a 0% interest second loan of up to $15,000.

- 75% of the loan is forgiven over a 10-year period.

- It can be used for down payments and closing costs.

- The home must be within San Antonio city limits.

Texas State Affordable Housing Corporation (TSAHC)

The TSAHC provides down payment assistance for “Texas Heroes” (teachers, police, veterans) and low-to-moderate income earners. This can be taken as a grant that never has to be repaid or a deferred forgivable second lien.

VA and FHA Loans

In a market with 80+ days of inventory, sellers are increasingly open to VA Loans San Antonio and FHA offers. These programs allow for zero to low down payments, which is essential as the median age of first-time buyers nationally has risen to 40.

Advice for Sellers: Why Homes are Sitting

If you are Selling a Home in San Antonio in 2026, you are no longer in a “list and wait” market. Homes are sitting longer because:

- Pricing Lag: Many sellers are still anchored to 2022 prices. The data shows that homes priced at market value are selling, while those over-testing the market are seeing significant days-on-market growth.

- Buyer Selectivity: With 6 months of inventory, buyers have the luxury of choice. They are prioritizing homes that are move-in ready or those offering seller concessions.

- Incentive Strategy: Offering a rate buydown (paying to lower the buyer’s interest rate) is often more effective than a price reduction in today’s environment.

The Way Forward: Strategy Over Headlines

If you are ready to buy, the most reliable advantage in 2026 will not come from waiting on a policy from Davos or Washington. It will come from understanding Bexar County Property Values and Comal County Real Estate Trends at the neighborhood level.

Today’s market offers a window of opportunity that didn’t exist two years ago. We have more inventory, more time for due diligence, and more room to negotiate. The mistake many make is waiting for the “perfect” moment, only to find that by the time it’s obvious, the competition has already returned.

Build your strategy around what you can control: your monthly payment comfort, your down payment assistance options, and a disciplined approach to finding the right home for your long-term needs.